Private equity firms are built around a partnership between two groups: General Partners (GPs) and Limited Partners (LPs).

GPs run the fund, and LPs provide most of the capital. The relationship between the two shapes every stage of the private equity process, from fundraising and investing to portfolio management and returns.

To understand GP vs LP in private equity, it helps to look at how each side participates across the private equity fund lifecycle.

What is a GP in Private Equity?

A General Partner is the private equity firm or fund manager that runs the fund and is responsible for turning investor capital into returns. Most GPs contribute a small amount of their own money to the fund, usually between 1% and 5%. This is called the GP commitment. It ensures that the GP has its own capital invested alongside its LPs.

What is an LP in Private Equity?

A Limited Partner is an investor that commits capital to the fund but does not manage it. LPs provide the majority of the fund's capital and rely on the GP to make investment decisions. Common LPs include pension funds, university endowments, sovereign wealth funds, insurance companies, family offices, foundations, and fund of funds.

GP vs LP in Private Equity: The Core Difference

Category | GP | LP |

Primary role | Manage the fund and investments | Provide capital to the fund |

Decision-making | Full control over investments and portfolio companies | Limited or no direct control |

Capital contribution | Usually, 1–5% of the fund | Usually, 95%+ of the fund |

Risk exposure | Reputation, career risk, and invested capital | Financial capital committed to the fund |

Compensation | Management fees and carried interest | Share of investment returns |

Day-to-day involvement | High | Low |

Liability | Unlimited or broader legal responsibility | Limited to the amount invested |

Main objective | Generate returns and raise future funds | Earn returns and preserve capital |

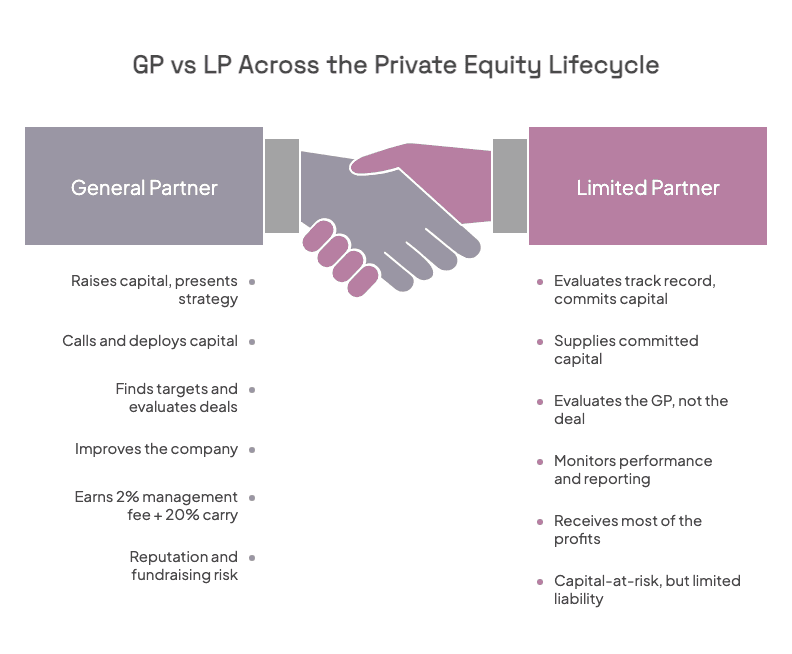

How GPs and LPs Participate Across the Private Equity Process

The clearest way to understand GP vs LP is to compare how each side plays different roles, contributes different resources, and takes on different levels of risk.

Fundraising: GPs raise capital, LPs commit it

Every private equity fund begins with fundraising. The GP creates the fund, develops the strategy, and approaches potential investors. The firm must explain what type of companies it plans to buy, how much capital it wants to raise, what returns it expects, and why LPs should trust the team.

The LP's role is to evaluate whether that fund deserves capital. LPs review the GP's track record, investment strategy, team stability, and prior performance. If the LP is satisfied, it commits capital to the fund.

Capital calls: LPs supply the capital, GPs deploy it

LPs do not transfer all of their capital at the start of the fund. Instead, they make a commitment. The GP then calls portions of that capital over time as investments are identified.

For example, an LP may commit $50 million to a fund. The GP may call only $10 million in the first year, another $15 million in the second year, and the remainder later.

The GP controls when and how capital is deployed. LPs are required to provide the requested amount when a capital call is issued. This structure benefits both sides. LPs can manage their liquidity more efficiently, while GPs avoid holding idle cash.

Deal sourcing: The GP leads, the LP observes

Finding attractive investments is entirely the GP's responsibility. Private equity firms spend significant time building relationships with investment bankers, founders, advisors, and executives. These relationships help the GP identify companies before they become widely marketed.

The LP does not participate directly in sourcing deals. However, some large LPs may review whether the GP has a strong pipeline and access to proprietary opportunities before deciding to invest. This is one reason why relationships matter so much in private equity. The best GPs often outperform because they see better deals earlier.

Due diligence: GPs evaluate the deal, LPs evaluate the GP

Once a target company is identified, the GP performs due diligence and decides whether to invest. The GP reviews the company's financial performance, market position, leadership team, legal risks, and growth potential. If the GP believes the business can generate attractive returns, it moves forward with the acquisition.

The LP does not approve individual deals in most private equity funds. Once the LP has committed capital, it gives the GP authority to make investment decisions.

This is one of the biggest differences between GPs and LPs:

GPs make the decisions.

LPs choose the managers who make those decisions.

Portfolio management: GPs improve, LPs monitor

After acquiring a company, the GP becomes actively involved in improving it. Depending on the investment, the GP may reduce costs, hire new management, expand into new markets, or complete acquisitions to improve the overall performance of the portfolio.

The GP's goal is to increase the company's value before eventually selling it.

The LP does not participate in the management of portfolio companies. Instead, LPs monitor how the GP is performing. Most GPs provide LPs with quarterly reports, annual meetings, and portfolio updates.

Large LPs may also sit on Limited Partner Advisory Committees, or LPACs, which review issues such as conflicts of interest, valuations, and fund extensions.

Returns and exits: Both sides benefit, but not equally

The final goal of every private equity fund is to sell investments at a profit. So when a portfolio company is sold, the proceeds are distributed between the GP and the LPs.

LPs receive most of the profits because they provided most of the capital. However, GPs also receive a share through carried interest.

A typical private equity fund follows a structure often called "2 and 20":

A 2% annual management fee

20% carried interest on profits

Management fees are paid to the GP every year regardless of performance. These fees cover salaries, research, travel, and operating expenses. For example, a $1 billion fund with a 2% management fee generates $20 million per year for the GP.

Carried interest works differently. In many private equity funds, LPs must first receive their original capital back and a preferred return, often around 8%, before the GP begins earning carried interest.

Only after that hurdle is met does the GP receive its share of the profits, typically 20%.

This structure is designed to align the GP's interests with the LP's interests. The GP earns meaningful rewards only if it generates strong returns.

Risk: GPs face broader liability, LPs face capital risk

Both GPs and LPs take risks, but the type of risk is different.

LPs face financial risk. They are committing large amounts of capital to a fund that may not perform as expected. If the investments fail, LPs may lose part of their investment. However, LP liability is limited. LPs can lose only the amount they committed to the fund.

GPs face greater exposure. In addition to investing some of their own capital in the fund, GPs may face legal and financial liability because they control the fund and make its decisions. While most firms structure the GP as a separate legal entity to limit personal liability, the GP still bears responsibility for regulatory issues, breaches of fiduciary duty, and other legal claims.

GPs also face reputational and fundraising risk. A GP that performs poorly may struggle to raise its next fund, lose investor trust, and damage its standing in the market.

For that reason, GPs are under constant pressure to generate returns, manage risk carefully, and maintain strong relationships with LPs.

Common Tensions Between GPs and LPs

Even when both sides want strong returns, GPs and LPs do not always agree. Many of the most common GP vs LP tensions arise around fees, transparency, and fund extensions.

Fees: LPs often push for lower management fees and lower carried interest, especially when committing large amounts of capital.

Transparency: LPs want more visibility into portfolio company performance. GPs may hesitate to share sensitive or highly detailed information.

Fund extensions: Private equity funds are often designed to last 10 years, but some investments take longer to exit. LPs may become frustrated if the GP requests multiple extensions.

Strategy drift: LPs invest based on a specific strategy. Problems arise when a GP begins pursuing deals outside its stated focus, such as moving into unfamiliar industries or geographies.

Performance pressure: If a fund underperforms, LPs may choose not to commit capital to the GP's next fund. In private equity, fundraising is heavily influenced by reputation and trust.

The Future of the GP-LP Relationship

The private equity industry is becoming more complex. Funds are larger, competition is stronger, and LPs expect faster, deeper insight into performance. As a result, successful GPs increasingly rely on better data, stronger relationship management, and more organized communication with their investors.

The firms that raise capital most successfully are usually not the firms with the largest networks. They are the firms that understand their relationships best. They know where warm introductions exist, which investors are most likely to commit again, and how investor sentiment is changing over time.

For many private equity firms, that information is still scattered across inboxes, spreadsheets, CRM notes, and individual team members. Rings AI brings it together in one place. It helps firms map GP-LP relationships, track every interaction, uncover warm paths to new investors, and manage fundraising more strategically.

As competition for capital continues to increase, better relationship intelligence becomes a real advantage. Book a demo with Rings AI to see how your firm can strengthen investor relationships and improve fundraising outcomes.