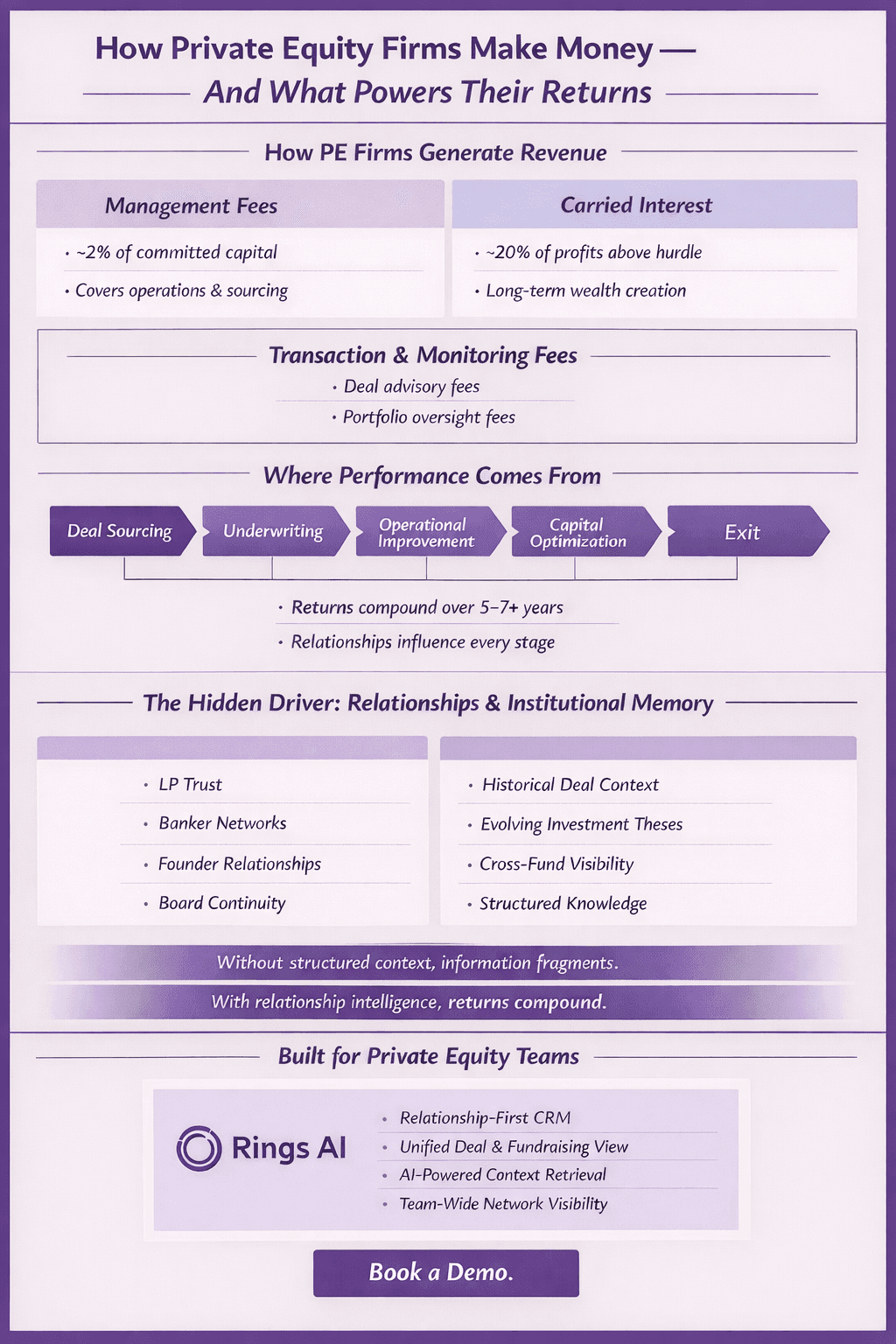

Private equity firms make money through a combination of management fees and performance-based returns on the capital they invest. At a basic level, firms earn annual fees for managing a fund and a share of the profits when portfolio companies are sold at a gain. That model sounds straightforward, but the mechanics behind it are anything but simple. Returns depend on disciplined deal selection, operational execution, capital structure decisions, and carefully timed exits.

What often gets overlooked is how relationship-driven this revenue model is. Fundraising depends on long-term LP trust. Deal flow depends on banker, founder, and operator networks. Portfolio outcomes depend on board dynamics and strategic alignment. Private equity economics are not powered by transactions alone; they are powered by sustained relationships and structured decision-making across years.

To understand how private equity firms truly make money, you have to look past the headline fee structure and examine how capital is raised, deployed, managed, and ultimately returned.

The sections below break down each revenue component and explain how they work together to shape the economics of a private equity firm.

Management Fees: The Revenue Base

Management fees form the predictable foundation of a private equity firm’s economics.

Most funds charge around 2% of committed capital annually, particularly in the early years of a fund’s lifecycle. These fees are designed to cover salaries, sourcing efforts, due diligence, portfolio oversight, and firm operations. While performance drives long-term wealth creation, management fees provide stability and allow the firm to operate consistently across multi-year investment cycles.

Industry data shows that fee structures remain a core component of private capital economics, even as pressure around performance and alignment continues to evolve. Management fees are not the primary profit engine, but they sustain the infrastructure required to generate returns.

For private equity teams, this predictable base revenue supports:

Investment professionals focused on sourcing and underwriting

Operating partners driving portfolio value creation

Fundraising teams managing LP relationships

Systems and processes that preserve the deal and portfolio context

The operational backbone funded by management fees directly influences how effectively a firm executes on deals and maintains LP trust. That infrastructure increasingly includes systems designed specifically for private equity workflows, rather than tools built for short-term sales cycles. A CRM built for private equity reflects the long timelines, overlapping fundraising cycles, and relationship depth that define the asset class. In this context, infrastructure is not optional. It protects both the firm’s management fee base and its long-term performance potential.

Carried Interest: Where Private Equity Firms Generate Real Wealth

Carried interest is the performance-based share of profits that private equity firms earn after returning capital to limited partners. In most traditional fund structures, firms receive around 20 percent of profits above a defined hurdle rate. Unlike management fees, which provide stability, carried interest reflects how effectively a firm selects, improves, and exits investments.

Data shows that long-term value creation, not short-term financial engineering, increasingly drives outperformance in private markets. Carried interest is directly tied to that sustained performance.

For private equity teams, carried interest depends on:

Disciplined deal sourcing and underwriting

Active portfolio value creation

Strategic capital structure management

Timing exists based on market conditions

Maintaining LP alignment throughout the fund lifecycle

Carried interest also reinforces why institutional context matters. Portfolio decisions often unfold over five to seven years, sometimes longer. Historical notes, board dynamics, and prior investment theses shape follow-on decisions and exit timing. Modern investment teams increasingly rely on systems that centralize this context rather than fragment it across inboxes and spreadsheets.

Carried interest rewards discipline over time. The infrastructure supporting that discipline often determines whether strong sourcing translates into realized returns.

Transaction and Monitoring Fees: Additional Revenue Streams

Beyond management fees and carried interest, many private equity firms generate revenue through transaction and monitoring fees.

Transaction fees are typically charged to portfolio companies at the time of acquisition or recapitalization, often structured as advisory or closing fees. Monitoring fees may be charged annually in exchange for strategic oversight, board participation, or operational guidance.

According to reporting from the U.S. Securities and Exchange Commission, fee transparency has become an increasing area of focus in private markets, particularly around how transaction and monitoring fees are disclosed and whether they are offset against management fees. Regulatory scrutiny has reinforced the importance of clear alignment between general partners and limited partners.

These fees can:

Supplement management fee revenue

Compensate firms for active portfolio involvement

Offset operational costs tied to value creation initiatives

Influence LP negotiations around fund economics

Transaction and monitoring fees highlight a broader point about private equity economics: revenue is layered and interconnected. Fundraising, portfolio oversight, compliance, and reporting often run in parallel. Structured data and centralized records become increasingly important when multiple revenue streams, reporting obligations, and stakeholder relationships overlap.

While these fees are typically smaller than carried interest in long-term impact, they form part of the overall economic model that supports sustained portfolio engagement and operational oversight.

How Private Equity Firms Increase Returns

Where fees explain how firms get paid, returns explain whether they build enduring franchises. Outperformance in private equity comes from disciplined capital deployment, active ownership, and timing exits with precision. The revenue model rewards firms that consistently convert sourcing advantage and operational involvement into realized gains.

In its Global Private Equity Report, Bain & Company shows that value creation increasingly comes from operational improvements rather than multiple expansions alone. Firms that drive margin expansion, revenue growth, and strategic repositioning tend to outperform those relying purely on financial structuring.

Private equity firms typically increase returns through:

Sourcing proprietary or differentiated deal flow

Underwriting with conservative downside protection

Driving operational improvements within portfolio companies

Optimizing capital structures to balance risk and return

Executing exits when market conditions support valuation

Execution across these areas depends on continuity. Investment theses evolve, board conversations influence strategic shifts, and LP expectations shape hold periods and distribution timing.

In private equity, return generation is cumulative. Each interaction, board update, and underwriting assumption feeds into the eventual exit value. Firms that manage that context deliberately tend to make sharper decisions over time.

Why Relationships Drive Private Equity Economics

Private equity is often described in financial terms, but its performance is deeply relationship-driven. Capital comes from limited partners who commit across multiple funds. Deals flow through bankers, founders, and operating executives who choose who to call. Portfolio outcomes depend on board alignment and trust built over years, not quarters.

Data from Preqin consistently shows that repeat fund managers with established LP relationships raise capital more efficiently than first-time managers. Fundraising success is not only about returns. It reflects credibility, transparency, and continuity.

Relationships influence private equity economics in several ways:

LP retention affects fundraising speed and fund size

Banker and intermediary networks shape proprietary deal access

Founder trust impacts exclusivity and negotiation leverage

Board dynamics influence operational execution and exit timing

These dynamics unfold across long timelines. Fundraising overlaps with portfolio management. The same relationship may appear in sourcing, diligence, governance, and eventual exit.

Systems that treat LPs and portfolio stakeholders as long-term relationships rather than transactional contacts better reflect how private equity firms actually operate.

In private equity, performance compounds through relationships. Firms that maintain structured visibility across those relationships protect both their capital base and their competitive edge.

Why Institutional Memory Matters in Private Equity

Private equity operates on long timelines. A relationship that begins during sourcing may resurface during a recapitalization years later.

An investment thesis debated in diligence may shape exit timing half a decade after closing. When context is lost between conversations, teams rely on recollection rather than record.

Institutional memory directly supports:

Consistent investment committee decision-making

Clear documentation of evolving theses

Continuity across partner transitions

Informed follow-on investments and exits

Without structured systems, historical context fragments across inboxes, spreadsheets, and personal notes. That’s the difference between generic CRM storage and relationship-centered intelligence.

Private equity returns are shaped by cumulative judgment. Institutional memory ensures that judgment improves with every cycle rather than resetting with each new fund.

Learn more about deal intelligence.

Why Private Equity Firms Use Rings AI

Private equity firms typically struggle with the fragmentation of information. Common challenges include: deal history that lives in the inbox, LP conversations that sit in scattered notes, and board context that disappears between funds. Over time, it weakens underwriting discipline and makes fundraising more reactive than strategic.

Most traditional CRMs were built for sales teams managing short pipelines. They track stages and activities well, but they seldom preserve the full relationship history that private equity depends on. When systems prioritize opportunities over enduring relationships, institutional memory slowly erodes.

Rings AI was built specifically for investors and deal-driven teams who operate across long cycles. It structures data around people and companies first, then connects deals, fundraising activity, and portfolio oversight into one shared record.

Key capabilities include:

Automatic capture of email and meeting history at the person and company level

Team-wide visibility into relationship depth and interaction history

Centralized notes and files linked across deals, LPs, and portfolio companies

AI-powered search and summaries across years of conversations

Unified deal and fundraising workflows inside the same system

Private equity returns compound through disciplined execution and durable relationships. Rings AI supports both by turning fragmented information into structured institutional memory.

If your firm’s economics depend on long-term context and consistent decision-making, see how Rings AI works in practice.

Rings AI helps private equity and venture capital teams manage relationships, deal flow, and portfolio data in one place. Book a demo to see how Rings AI supports your investment workflow.