Private equity fundraising is the process of raising capital from investors for a private equity fund.

The fund manager, also called the general partner (GP), gathers commitments from institutional and high-net-worth investors, known as limited partners (LPs), and uses that capital to invest in private companies.

Raising a private equity fund is often harder than sourcing deals. LPs are not only evaluating your returns. They are deciding whether they trust your team, your strategy, and your ability to manage capital over the next decade.

A successful fundraising process requires preparation, relationship management, and a clear understanding of what LPs want.

What is Private Equity Fundraising?

A private equity fund does not raise money deal by deal. Instead, the GP raises a pool of capital upfront. LPs commit a certain amount to the fund, and the GP calls that capital over time as investments are made.

Most private equity funds have a lifecycle of around 10 years:

Years 1–5: The GP invests capital into companies

Years 5–10: The GP works to improve and exit those investments

After exits: Profits are distributed back to LPs

The fundraising process itself usually begins 6–18 months before the first close of the fund.

Private equity firms typically raise capital from pension funds, endowments, family offices, funds of funds, high-net-worth individuals, sovereign wealth funds, and insurance companies.

Unlike venture capital, where investors may back early-stage growth stories, private equity investors usually expect more predictable returns, stronger processes, and a well-defined investment strategy.

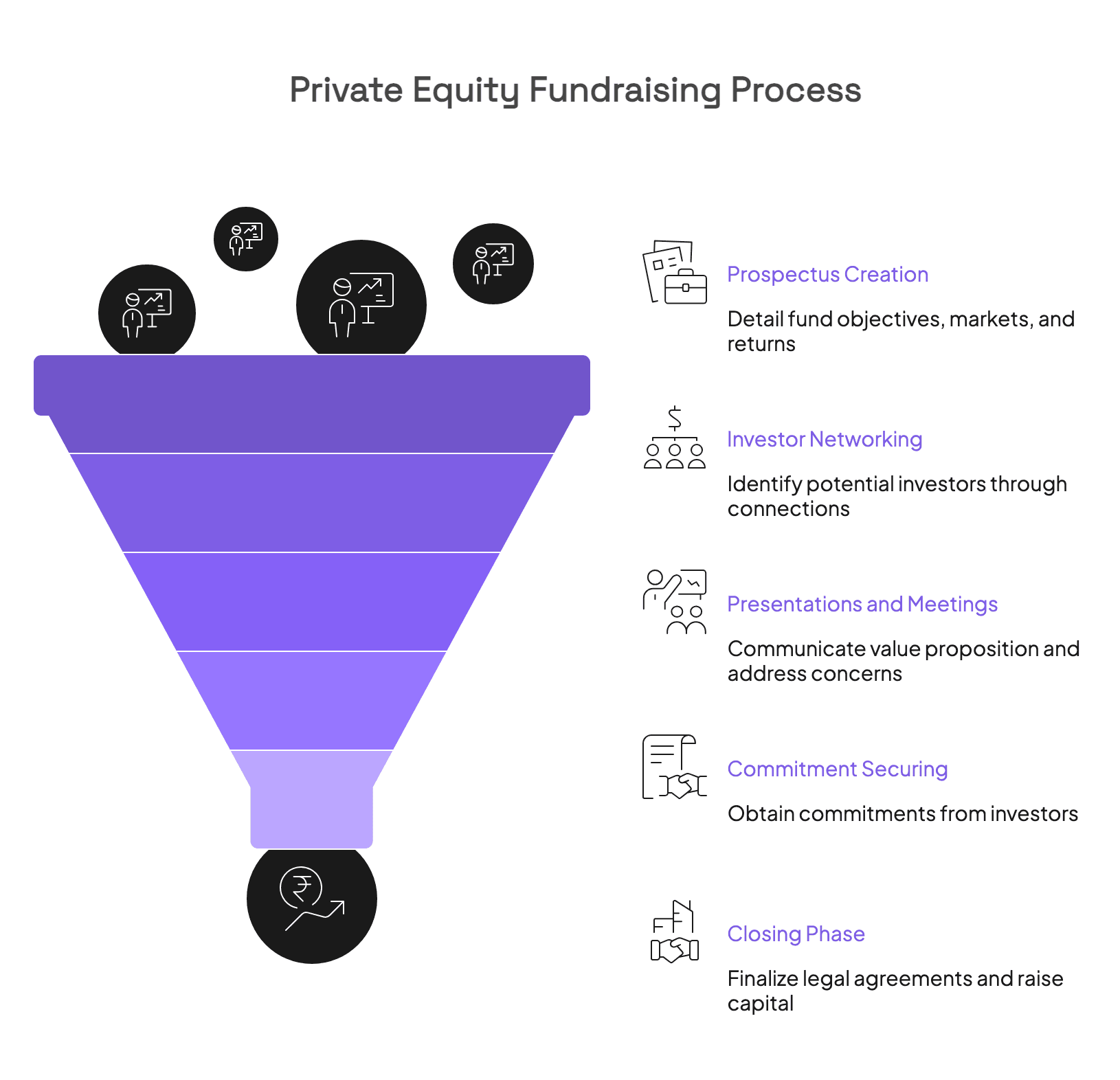

How the Private Equity Fundraising Process Works

While every firm runs its process differently, most private equity fundraising efforts follow the same stages.

1. Define your fund strategy

Before approaching investors, you need a clear investment thesis. LPs want to understand which companies you invest in, which sectors and geographies you focus on, what your typical deal size looks like, and how you create value after acquisition.

For example, your strategy may be:

"We acquire founder-owned manufacturing businesses in North America with EBITDA between $5 million and $20 million, then improve operations and expand geographically."

The more specific your strategy is, the easier it becomes for LPs to understand why your fund exists and where you can generate returns. A vague strategy, such as “we invest in good companies,” is difficult to differentiate and rarely resonates with investors.

2. Determine the fund size

The next step is deciding how much capital to raise. Your target fund size should match your strategy.

If you plan to acquire mid-sized businesses with enterprise values between $50 million and $100 million, a $25 million fund is probably too small. On the other hand, raising a fund that is much larger than your opportunity set can create pressure to make weaker investments.

Most first-time and emerging managers start smaller, then grow fund size over time as they build a track record.

For example:

First fund: $50 million–$100 million

Second fund: $150 million–$300 million

Later funds: Larger based on performance and LP demand

LPs generally prefer to see discipline. It is often better to raise a smaller fund successfully than to spend two years chasing an unrealistic target.

3. Build your fundraising materials

Investors will expect a clear, professional set of fundraising documents. These usually include a private placement memorandum (PPM), due diligence questionnaire (DDQ), financial track record, and sample deal case studies.

Your fundraising deck should answer five core questions:

Why does this fund exist?

Why is now the right time for this strategy?

Why is your team the right team to execute it?

How have you performed in the past?

What returns can LPs reasonably expect?

Like a good sales proposal, your fundraising materials need to explain the problem, your solution, and why your approach is credible and easy to understand. Clear structure and concise communication often matter more than lengthy detail.

What LPs Look for When Deciding to Invest

Private equity investors rarely commit capital based on returns alone. They are evaluating the entire firm. The main factors LPs look for include:

Track record

This is usually the single most important factor. LPs want evidence that you have sourced attractive deals, improved businesses after acquisition, generated strong returns, and managed downside risk.

If you are a first-time fund manager without a formal track record, you can still demonstrate credibility through deals completed at previous firms, sector expertise, advisory work, and angel or personal investments.

Team quality

LPs invest in people as much as they invest in strategy. They want to understand who is on the team, how long they have worked together, what experience they bring, and whether their skills complement one another.

For example, a team with one partner focused on sourcing and another with deep operational experience will often appear stronger than a team with overlapping backgrounds.

LPs also care about stability. If key team members leave frequently or responsibilities are unclear, investors may hesitate.

Differentiation

The private equity market is crowded, and LPs may review dozens of funds each year that all promise strong returns. To stand out, you need a clear reason for investors to remember you.

That differentiation might come from deep expertise in a niche industry, access to proprietary deal flow, unique operating capabilities, a strong regional network, or the ability to source off-market opportunities.

The strongest fundraising stories are usually simple and specific.

For example, “We are former healthcare operators who buy small medical device companies and help them expand into new markets” is much easier for LPs to understand and trust than a broad, generic buyout strategy.

Alignment of interests

LPs want to know that your incentives are aligned with theirs. They typically look at the GP’s own capital commitment, the management fee structure, carried interest, and the overall economics of the fund.

Most LPs expect the GP to commit at least 1–5% of the fund because it shows confidence and ensures the team has meaningful capital at risk alongside investors.

Fundraising Is Won Through Relationships, Not Outreach

Private equity fundraising is built on relationships, not cold outreach. Most LPs commit only after multiple conversations over time, often because they were introduced through someone they already trust, such as a founder, advisor, banker, or existing investor.

That makes relationship management just as important as the investment strategy itself. Firms need to know which LPs they have already spoken with, who introduced them, which investors are most engaged, and where follow-up is needed.

Once a fundraising process involves dozens of LPs and many months of conversations, tracking all of that manually becomes difficult.

Rings AI helps private equity firms keep a live view of their investor network, identify warm introductions, and organize every conversation in one place.

That makes it easier to prioritize the right relationships, follow up at the right time, and move fundraising forward with more structure and confidence.

Common Challenges in Private Equity Fundraising

Even strong private equity firms face obstacles during fundraising. The process is often longer, more relationship-driven, and more complex than managers expect.

Long timelines

Private equity fundraising often takes 12 to 18 months, sometimes longer. LPs move slowly because they need time to review materials, meet the team, compare opportunities, complete due diligence, and secure internal approvals.

As a result, firms need to begin fundraising earlier than they think and maintain consistent communication throughout the process.

Limited existing network

First-time and emerging managers often struggle because they do not yet have an established LP network. They may need to rely on personal contacts, former colleagues, placement agents, and industry relationships to get initial meetings.

Having network mapping software can help firms identify which contacts are most likely to lead to warm introductions and which investors are already connected to their broader network.

Weak positioning

Many funds fail to raise capital not because the strategy is weak, but because the story is unclear. If LPs cannot quickly understand what the fund does, why the team is different, and why now is the right time to invest, they are unlikely to move forward.

A strong investment thesis solves this problem by clearly connecting your strategy, market opportunity, and edge as a team. We cover this in more detail in our guide on how to write an investment thesis that investors can understand, trust, and remember.

Poor follow-up

Fundraising usually involves dozens or even hundreds of conversations. Without a structured process, firms can easily lose track of meetings, introductions, next steps, and investor interest levels.

A relationship management platform for PEs helps firms keep every conversation, follow-up, and action item in one place, making it easier to stay organized and move investors through the fundraising process more consistently.

Create a More Structured Approach to Fundraising

Private equity fundraising is about more than presenting an attractive investment strategy. LPs are evaluating whether they trust your team, whether your approach is differentiated, and whether you can execute consistently over many years.

The firms that raise capital most effectively are usually the ones that stay organized, communicate clearly, and build strong relationships long before they ask for commitments.

As fundraising becomes more complex, firms need a better way to manage relationships and stay organized. Rings AI helps private equity firms do that by bringing investor conversations, introductions, and activity into one place.

If you want a more structured and predictable fundraising process, book a demo with Rings AI.