In simple terms, a leveraged buyout (LBO) is the acquisition of a company using a large amount of borrowed money. Instead of paying for the entire purchase with their own capital, the buyer finances most of the deal with debt and uses the company being acquired as collateral.

Private equity firms are the most common buyers in leveraged buyouts. They use LBOs to acquire mature businesses, improve performance, grow profitability, and eventually sell the company for more than they paid.

In this guide, we’ll explain how a leveraged buyout works, why firms use it and risks involved, and how private equity teams can streamline the process with better relationship visibility and deal intelligence.

How a Leveraged Buyout Works

A leveraged buyout works by combining three main ingredients:

Equity from the buyer

Debt from lenders

Cash flow from the target company

The buyer identifies a company with stable revenue, predictable cash flow, and assets that can support borrowing. They then structure the acquisition using a mix of debt and equity.

In a typical leveraged buyout, the buyer may contribute only 10% to 30% of the purchase price from their own funds, while the remaining amount comes from bank loans, bonds, or other forms of financing.

For example, imagine a company is worth $100 million. A private equity firm might contribute $25 million of equity and borrow the remaining $75 million. After the deal closes, the company itself becomes responsible for repaying that debt.

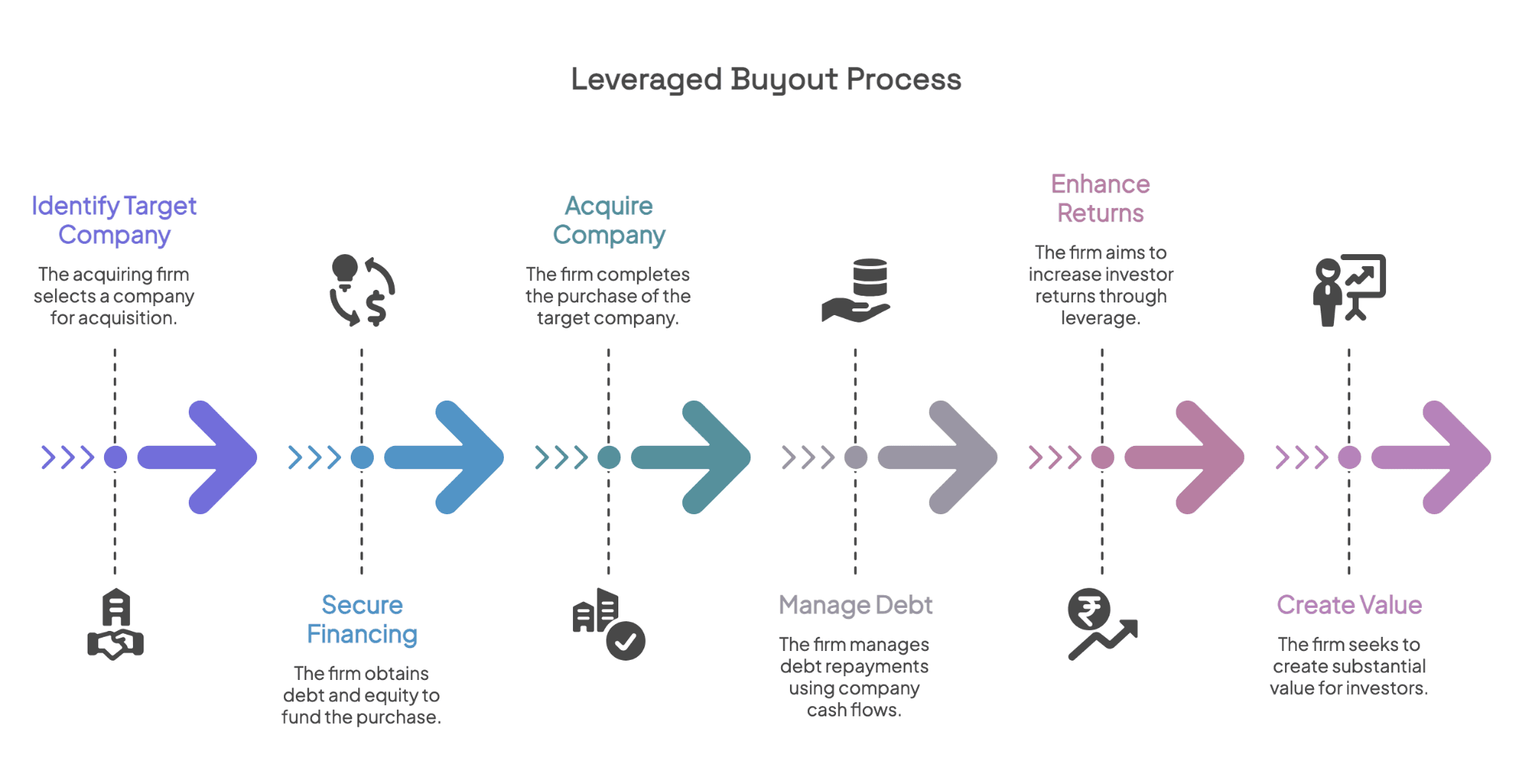

The process usually happens in six stages:

Step 1: Raise capital from limited partners (LPs)

Before a private equity firm can pursue an LBO, it raises capital from limited partners, such as pension funds, endowments, family offices, insurance companies, and wealthy individuals.

These investors commit money to the private equity fund, which the firm later uses to acquire companies. Fundraising can take months and often depends on the firm's track record, investment strategy, and relationships with investors.

Many firms use relationship intelligence software to centralize LP notes, meeting history, and investor relationships.

Step 2: Source and evaluate target companies

Once capital has been raised, the firm begins searching for companies that fit the profile of a strong leveraged buyout target.

Most buyers look for companies with predictable cash flow, low existing debt, strong market positions, and opportunities to improve operations. The firm then reviews the company's financials, leadership team, industry, and future growth potential before deciding whether to move forward.

Step 3: Arrange debt financing

After identifying a target, the buyer works with banks and lenders to structure the financing. Most LBOs use a mix of senior debt, mezzanine debt, high-yield bonds, and sometimes seller financing options.

Senior debt: Lowest-risk debt with first claim on the company’s assets and cash flow.

Mezzanine debt: Higher-risk debt with higher returns, often including ownership rights.

High-yield bonds: Also called junk bonds, it’s large-scale financing with higher interest rates.

Seller financing: The seller agrees to receive part of the payment over time.

At this stage, firms often have conversations with several lenders at once. Keeping track of previous lender relationships, financing terms, and deal notes can help speed up negotiations and make it easier to return to lenders that have financed similar transactions before.

Step 4: Complete the acquisition

Once financing is secured, the deal closes. Ownership transfers to the buyer, and the company becomes responsible for repaying the debt.

This stage involves close coordination between lawyers, lenders, management teams, advisors, and board members. Firms need a clear record of every stakeholder, conversation, and next step so the transaction stays organized and avoids delays.

Step 5: Improve the company and repay the debt

After the acquisition, the private equity firm works to increase the company's value. That may involve reducing costs, improving operations, entering new markets, or replacing management.

As the company generates cash flow, it uses that cash to pay down the acquisition debt. The more debt the company repays, the more valuable the buyer's equity becomes.

Step 6: Exit through a sale or IPO

When the company has increased in value, and much of the debt has been repaid, the private equity firm exits the investment. This usually happens through a sale to another company, another private equity firm, or an IPO.

The less debt remaining at exit and the higher the company's value, the stronger the return.

A Real-World Leveraged Buyout Example

One of the most famous leveraged buyouts in history was the acquisition of RJR Nabisco in 1989.

RJR Nabisco was acquired by KKR in a deal worth approximately $25 billion.

At the time, it was the largest leveraged buyout ever completed. KKR, formerly Kohlberg Kravis Roberts, financed most of the purchase with debt, betting that the company would generate enough cash to repay it.

The deal became famous because of its size, complexity, and the competition between bidders. It was later chronicled in the book Barbarians at the Gate.

More recent examples include private equity acquisitions of software, healthcare, and business services companies. These businesses are attractive because they often produce predictable cash flow that can support debt repayment.

Why Buyers Use Leveraged Buyouts

Buyers use leveraged buyouts because they allow them to control a large company without committing all of their own money.

Instead of needing $500 million to buy a company outright, a private equity firm may only need $100 million to $150 million of equity and can borrow the rest. That allows the firm to pursue larger acquisitions and potentially earn higher returns.

There are several reasons why leveraged buyouts are attractive:

Higher returns on equity

Because the buyer invests less of their own capital, even modest growth in the company's value can create outsized returns.

For example, if a buyer invests $20 million in equity and later sells the business for a gain of $40 million, they have doubled their money. If they had invested the full purchase price themselves, the return would be much smaller.

Ability to acquire larger companies

Debt allows buyers to pursue acquisitions that would otherwise be too expensive. This is particularly important for private equity firms that manage capital on behalf of investors.

Tax benefits

Interest payments on debt are usually tax-deductible. That lowers the company's taxable income and can make the overall deal more financially attractive.

Pressure to improve performance

High debt levels force management to operate efficiently. The company must generate enough cash to meet its debt obligations, which often leads to tighter cost control, operational improvements, and stronger financial discipline.

Risks of a Leveraged Buyout

Despite their potential benefits, leveraged buyouts carry meaningful risks.

Too much debt

The biggest risk is that the company cannot support its debt burden. If revenue falls or costs rise unexpectedly, the company may struggle to make its loan payments. This is especially dangerous during recessions or industry downturns.

Limited flexibility

A heavily indebted company has less flexibility to invest in growth, hire new employees, or respond to changing market conditions. Instead of spending money on new products or expansion, management may have to focus primarily on repaying debt.

Higher financial risk

LBOs magnify both gains and losses. If the company performs well, returns can be very high. If the company performs poorly, the buyer may lose a significant amount of money.

Employee and cultural challenges

Private equity firms often reduce costs after an acquisition. That may involve restructuring, layoffs, or leadership changes. While these steps can improve profitability, they may also create uncertainty and lower morale inside the company.

How Private Equity Firms Evaluate LBO Opportunities

Private equity firms rarely pursue an LBO based on financial statements alone. They also evaluate:

The quality of the management team

Industry trends and competitive pressure

Potential operational improvements

Exit opportunities in the future

Existing relationships with lenders, advisors, and investors

In practice, many firms spend as much time assessing the people around a deal as they do assessing the company itself.

This is where relationship intelligence becomes valuable. Platforms like Rings AI help private equity firms map relationships across founders, bankers, investors, and operators so they can identify the right connections faster and move opportunities forward with more confidence.

Rings AI also enriches contacts and companies with more than 100 million data points updated daily, giving firms access to real-time deal intelligence across investors, lenders, companies, and markets. Teams can see recent company developments, prior transactions, lender activity, investor interests, and similar deals before deciding where to focus.

With notes, meetings, emails, and files stored in one centralized platform, firms can keep every conversation tied to the right opportunity and move faster with more confidence.

The Key to a Successful Leveraged Buyout

A successful leveraged buyout depends on more than capital and debt. Firms also need the right relationships, the right timing, and a clear understanding of the people and companies involved.

The firms that win deals are often the ones that identify opportunities earlier, build stronger connections, and move with more confidence throughout the process.

Book a demo with Rings AI to see how it can support your next acquisition.