Private equity firms spend a great deal of time discussing performance, but not all performance metrics tell the same story.

Two of the most common metrics are DPI and IRR. Both are used by general partners and limited partners to evaluate a fund, yet they measure very different things. One tells you how much cash has actually been returned. The other tells you how quickly value was created.

Because of that, it is common to see a fund with a strong IRR but weak DPI, or vice versa. The DPI vs IRR debate exists because the two metrics answer different questions about fund performance. A manager may claim success based on one metric while investors focus on the other.

The more important question is not whether DPI or IRR is “better.” The real question is: what are you trying to understand?

What is DPI?

DPI, or distributed to paid-in capital, measures the amount of capital returned to investors relative to the amount they contributed.

The formula is simple:

DPI = Cumulative Distributions/Paid-in Capital

If a fund calls $100 million and later distributes $150 million, its DPI is 1.5x.

A DPI of:

1.0x means investors have received back exactly what they invested

Above 1.0x means the fund has generated realized gains

Below 1.0x means the fund has not yet returned all invested capital

What makes DPI useful is that it only counts realized cash. It ignores unrealized portfolio value and paper gains.

What is IRR?

IRR, or internal rate of return, measures the annualized return of a fund while accounting for the timing of cash flows.

Unlike DPI, IRR is sensitive to when money is invested and when it is returned. A fund that returns capital quickly can generate a high IRR even if the total amount returned is relatively modest.

For example:

Fund A turns $100 million into $150 million in three years

Fund B turns $100 million into $200 million in eight years

Fund B created more value overall. But Fund A is likely to report the higher IRR because it returned money faster.

IRR is essentially the discount rate that makes the net present value of all cash flows equal to zero, which is why small differences in timing can have a major impact on reported performance.

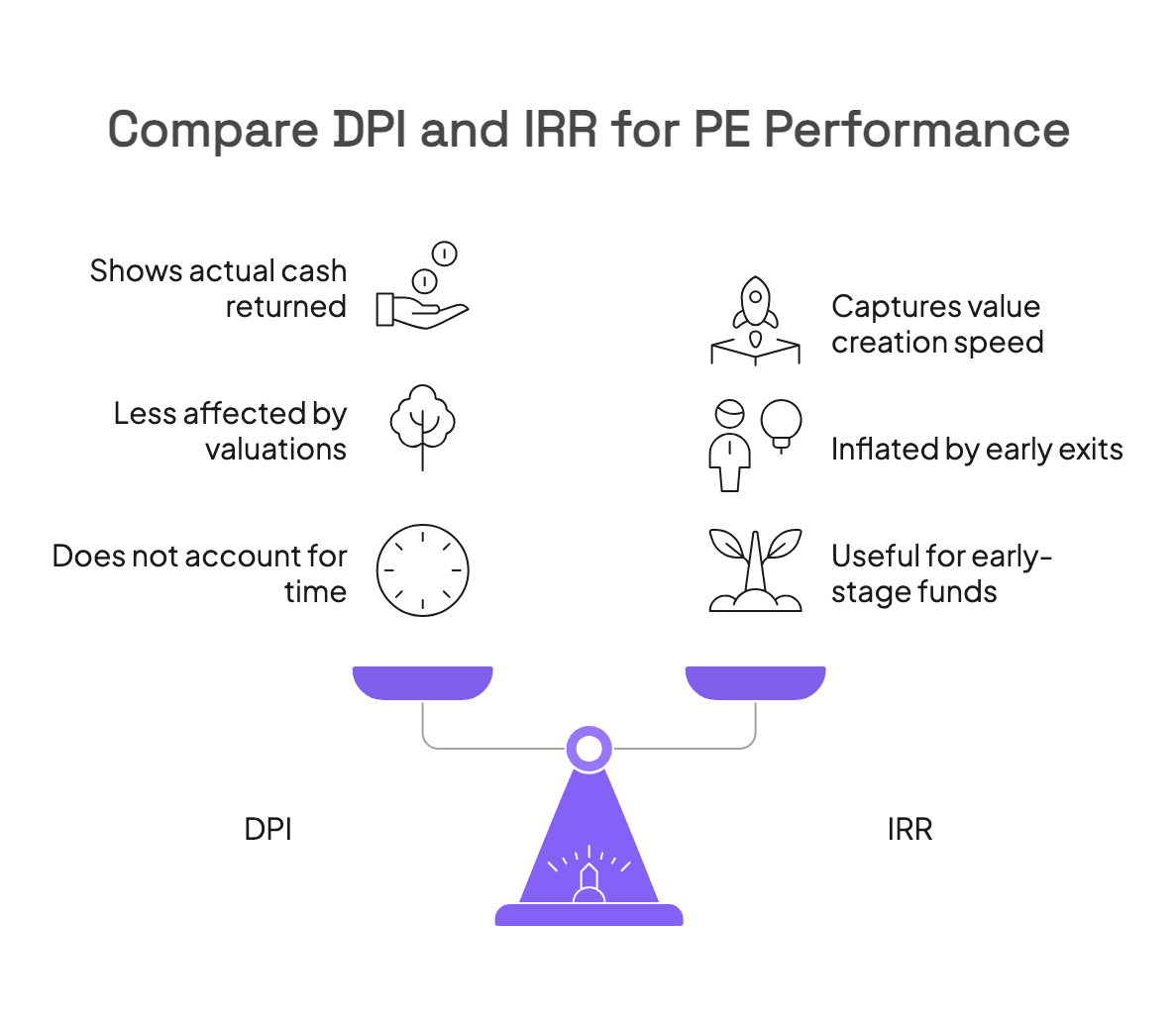

DPI vs IRR: Why These Metrics Tell Different Stories

The reason these metrics sometimes conflict is simple:

DPI measures the magnitude of returns

IRR measures the speed of returns

Consider these examples:

Fund | Paid-In Capital | Distributions | DPI | Time to Return | IRR |

Fund A | $100M | $150M | 1.5x | 2 years | 22% |

Fund B | $100M | $200M | 2.0x | 8 years | 9% |

Fund A appears stronger if you focus on IRR because it returns capital more quickly. Fund B appears stronger if you focus on DPI because it ultimately returns more cash to investors.

Neither view is wrong. They simply answer different questions.

IRR asks: “How efficiently did the fund generate returns?”

DPI asks: “How much money did investors actually get back?”

Most investors also review TVPI and RVPI alongside DPI and IRR to understand both realized and unrealized value.

Which Metric Matters More at Different Stages of a Fund?

In the DPI vs IRR debate, the more useful metric often depends on where the fund is in its lifecycle.

Early fund life: IRR matters more

In the first few years, funds usually have little DPI because investments are still being built. At this stage, investors rely more heavily on IRR and unrealized value to understand whether the strategy is working.

A strong early IRR may indicate that the fund is sourcing well, improving portfolio companies, and creating value.

Mature fund life: DPI matters more

As the fund approaches the end of its life, the DPI vs IRR balance usually shifts toward DPI. By this point, investors expect to see actual exits and actual cash distributions.

A mature fund with high IRR but weak DPI may indicate that unrealized gains have not yet translated into cash returns. Over time, realized cash becomes more important than projected value.

Common Mistakes in the DPI vs IRR Debate

Much of the confusion around DPI vs IRR comes from relying too heavily on one metric and ignoring the other. Both metrics are useful, but they can be misleading when viewed in isolation.

Over-relying on IRR

IRR can sometimes overstate performance. A single early exit can push IRR sharply higher, even if the rest of the portfolio underperforms.

IRR can also be inflated by:

Subscription lines that delay capital calls

Unrealized portfolio valuations

Short holding periods

As a result, a high IRR does not always mean a fund has produced strong realized returns.

Over-relying on DPI

DPI has its own limitations. It doesn’t tell you how long it took to generate returns. A 2.0x DPI achieved in five years is very different from a 2.0x DPI achieved in ten years.

DPI can also make strong young funds appear weaker than they are because most of the value may still sit in unrealized portfolio companies.

The Best Approach: Use Both Together

The best way to approach DPI vs IRR is not to choose between them, but to use both. A high-quality private equity fund generally has:

Strong IRR early in the fund lifecycle

Growing DPI as exits begin

A healthy balance between realized and unrealized value

When both metrics are moving in the right direction, investors gain confidence that the fund is creating value and successfully converting that value into cash.

A useful framework is:

Use IRR to understand efficiency and momentum

Use DPI to understand realized performance and credibility

Use TVPI and RVPI to understand what remains

Turning Portfolio Data Into Better Investment Decisions With Rings AI

DPI and IRR are ultimately the result of thousands of decisions made throughout the life of an investment. Improving IRR depends on identifying issues early, moving quickly, and exiting at the right time. Improving DPI depends on turning portfolio value into realized cash returns.

To do that consistently, firms need more than quarterly reports and scattered spreadsheets. They need a clear, real-time view of how each portfolio company is performing, where risks are emerging, and which investments may be approaching an exit window.

Without the right systems, critical information is often spread across emails, board decks, operating reports, and conversations with management teams. That makes it harder to spot underperformance, identify opportunities, and act before returns are affected.

The right technology gives private equity firms the visibility to make more informed decisions across the portfolio.

Rings AI helps firms centralize portfolio monitoring, company updates, relationship intelligence, and operating KPIs in one place. With a clearer view of what is happening across the portfolio, firms can:

Identify underperforming companies earlier

Monitor the metrics most likely to influence future returns

Recognize potential exit opportunities sooner

Stay closer to management teams, advisors, and buyers

Make faster, more informed decisions that can improve both IRR and DPI over time

Better portfolio visibility does not guarantee stronger returns. But it gives firms a much better chance of creating them.

Book a demo to see how Rings AI supports smarter private equity decision-making.